Creation of value through sustainability, myth or reality?

Sustainability has gone through a cycle of inflated expectations, disillusionment, and polarization. However, the evidence shows that when it focuses on financially material issues, sustainability drives real value creation.

By Gema Esteban. Originally published in Spanish in Newsletter #27 of the Esade Center for Corporate Governance Center. Subscribe here.

Over the past 10 years, sustainability has followed a trajectory similar to the “Gartner Hype Cycle,” which explains the path an emerging technology takes from its initial emergence to widespread adoption. We could say that the “Peak of Inflated Expectations” was reached during COP 26, when the financial sector as a whole, led by BlackRock, began to support the climate transition and created initiatives to facilitate investment flows toward ESG. And then Trump arrived and accelerated the “Trough of Disillusionment,” where we currently find ourselves.

The evolution of ESG as a trend probably needed time to develop and mature. But the reality is that, far from stabilizing, it is now more polarized than ever. The introduction of the EU’s omnibus package has reduced sustainability reporting and due diligence obligations for companies, creating on the one hand uncertainty and confusion for firms and investors, and on the other, rationalizing reporting requirements. In the United States, regulation varies from state to state. In the investment world, asset managers have faced increased scrutiny of their sustainability-related practices, whether for “greenwashing” or for focusing on factors not considered financially material. This has heightened the divergence between European and US investors’ approaches to these issues. The world’s two main proxy advisors have taken almost opposite directions: on February 11, 2025, ISS announced that it would “indefinitely suspend” consideration of gender, racial, and ethnic diversity on US corporate boards when issuing its voting recommendations. Glass Lewis, meanwhile, maintained its policies for the 2025 season, marking with a “Diversity Alert” any report including a negative recommendation related to a director’s diversity.

So what should board members and corporate executives do? How should they now approach Sustainability/ESG? How can they separate the signal from the noise?

The Rosetta Stone

On September 27, 1822, French linguist Jean-François Champollion announced in Paris that he had deciphered the mystery of hieroglyphics thanks to a second-century BC stele—an inflection point that effectively launched modern Egyptology and established rigorous standards for comparative linguistics. By aligning hieroglyphic, demotic, and Greek, the Rosetta Stone provided a systematic key that validated cross-correlation methods still used in cryptanalysis, data translation, and interdisciplinary research. Its impact extended beyond academia, influencing museum practice, cultural heritage stewardship, and a more nuanced global narrative on ancient innovation, governance, and spirituality. The discovery and deciphering of the Rosetta Stone redefined global knowledge, transforming a silent civilization into a readable archive of governance, beliefs, art, and everyday life that had been inaccessible for more than a millennium.

The Rosetta Stone analogy presents ESG as a trilingual key to translate environmental, social, and governance commitments into economic terms that operators, financiers, and customers can all read in the same way. Read this “stone” so that energy efficiency corresponds to gross-margin expansion, worker safety to uptime and supply-chain continuity, and board oversight to a lower cost of capital and faster decision-making—recasting ideology as materiality, operational discipline, and risk-adjusted returns, aligned with strategic direction and performance expectations for executives. But is this possible?

Value-creation framework

Not only is it possible; it is also well documented: focusing on financially material ESG issues is associated with superior stock-market performance relative to peers, while focusing on immaterial issues does not produce the same effect. Companies with integrated sustainability practices also outperform in the long term on both market and accounting metrics compared to those that do not.

Investors expect sustainability to play an even greater role in financial performance going forward, with decarbonization, waste and circularity, and human rights and digital responsibility gaining importance. Yet many organizations struggle to turn sustainability into action and link it to financial outcomes. Key challenges include demonstrating the financial impact of these initiatives, securing shareholder and investor support, and addressing gaps in corporate governance and process and capability integration. A data-driven approach with clear KPIs and ROI metrics can be essential for building the business case, driving adoption, and unlocking sustainability’s full value potential.

Ultimately, investor frameworks and sustainable-investment strategies aim to capture value that is sometimes intangible and does not translate easily into traditional financial models. Because how can a company’s excellent employee experience be explicitly translated into its EBITDA or its multiple? While it should be an indicator of excellence—and therefore be reflected in company results—putting a number on it is not straightforward. Renowned academics such as Harvard’s George Serafeim or Oxford’s Robert Eccles have written extensively on how to integrate ESG into corporate strategy to turn it into a value generator. Driving value creation linked to sustainability must be a continuous journey, supported by key organizational enablers at company level. Multiple academic studies also show predominantly non-negative and often positive relationships between ESG and financial performance, especially over longer horizons and when measured through operational drivers rather than disclosure alone.

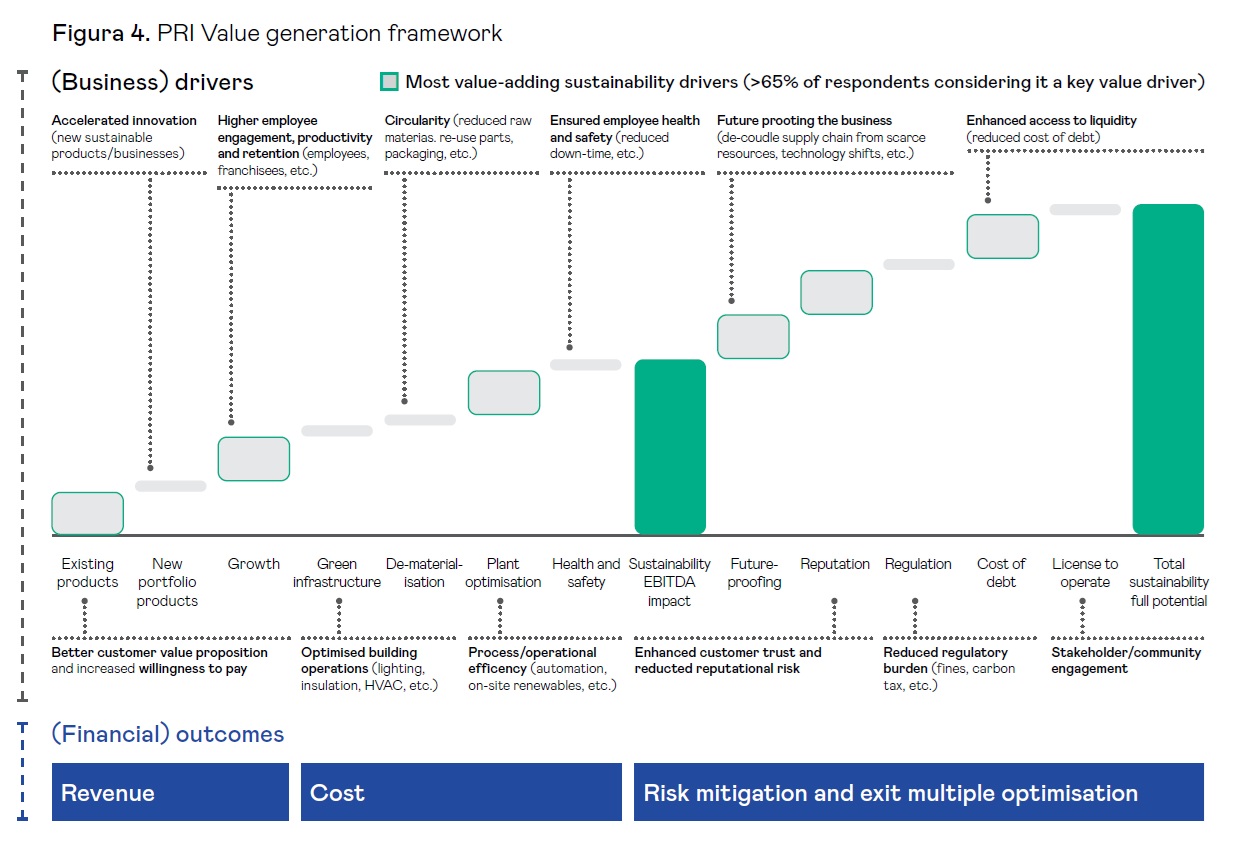

In late 2024, PRI—together with Bain & Company and NYU Stern—launched a major global project on value creation through sustainability, aimed at developing methodologies and practical guidelines to quantify the financial impact of sustainability initiatives in specific sectors. More than 400 investors participated through surveys, interviews, and workshops across various regions of the world. Below we explore this framework, which is highly practical and focused. It begins with an analytical structure based on four stages: identifying material issues, the associated initiatives, the business drivers, and finally, quantification.

1. Identifyingmaterial issues

First, it is essential to identify the material sustainability issues that entail risks and opportunities under a double-materiality lens, while giving priority to those with clear financial materiality for the business model and capital formation across different time horizons, in order to anchor the strategy and guide resource allocation. This assessment should operate as the backbone of the strategy by recognizing both the externalities and the outcomes of the business model that translate into tangible and verifiable financial effects. It is a demanding exercise, but one that is useful for articulating a truly integrated strategy. As an illustration, consider the data-center industry, the core infrastructure of one of the major technological currents of our time: artificial intelligence.

Possible material issues for data centers (non-exhaustive):

- Energy efficiency and power usage effectiveness (PUE).

- Grid sourcing and on-site renewable generation.

- Attraction, development, and retention of scarce technical talent.

- Water management and thermal control.

- Physical and climate-transition risks affecting facilities.

2. Designing targeted initiatives

Second, it is advisable to articulate a coherent and prioritized set of initiatives that are closely linked to the previously prioritized issues, ensuring that each action has a clear rationale within the strategic logic that underpins it. This portfolio should be rooted in the operational reality of both the sector and the organization itself, prioritizing pragmatic interventions with clear scope and explicit causal hypotheses between activity and outcome. Focus requires translating each initiative into verifiable objectives, defined resources, and traceable accountabilities, avoiding tactical dispersion and redundancies. At the same time, contextual adaptation requires calibrating technologies, processes, and execution pace according to the maturity of business units and prevailing regulatory and competitive constraints. Only then can strategic ambition translate into coherent, measurable, and learnable actions.

Possible initiatives for data centers (non-exhaustive):

- Modernize cooling systems, airflow management, and control systems to improve PUE.

- Procure renewable energy (PPAs) and deploy on-site solar with storage.

- Implement demand response and load shifting to reduce peak-time costs.

- Launch differentiated talent programs: apprenticeships, upskilling, and career paths to mitigate scarcity risks.

- Adopt water-efficient cooling solutions and recycling technologies where viable.

3. Mapping business drivers

It is important to rigorously identify the monetizable benefits and risk mitigations that each initiative can deliver—operational efficiency, customer loyalty and retention, revenue growth, regulatory preparedness, financing conditions—in alignment with strategic frameworks that link materially financial ESG factors with value creation. This impact mapping must distinguish between direct and indirect effects, their probability and magnitude, and the time horizon in which they materialize, as well as the operational and financial transmission mechanisms that translate them into margins, cash flows, and cost of capital. Only then is it possible to build verifiable business cases, prioritize investments based on materiality, and support accountability toward the market and stakeholders. Ultimately, the traceability between a material ESG lever and an economic outcome constitutes the load-bearing structure of a genuinely value-oriented strategy.

Possible business drivers for data centers (non-exhaustive):

- Lower energy intensity and optimized building operations thanks to upgrades.

- New revenues or savings derived from demand response and utility incentives.

- Lower turnover and fewer hiring delays thanks to a stronger talent pipeline.

- Greater resilience and fewer disruptions due to diversified energy sources.

- Preferential access to capital due to improved ESG risk profiles.

4. Quantifying financial outcomes

Finally, the exercise must culminate in translating the drivers into traceable financial outcomes linked to P&L, balance sheet, and cash flow, with baselines, targets, and time horizons, reflecting the evidence that ESG integration improves decision-making quality and risk-return profiles when it is connected to material fundamentals and metrics.

Possible financial outcomes for data centers (non-exhaustive):

- OPEX reduction through energy savings and maintenance optimization.

- Deferred CAPEX through extended asset life and modular upgrades.

- Lower cost of capital or insurance premiums through risk mitigation.

- Revenue increases from premium low-carbon services and higher utilization.

- Lower training and replacement costs due to improved retention.

But this is not enough: senior-management leadership, robust data collection, investor involvement, effective decision-making, and adequate capabilities across departments are all critical to success—and remain common bottlenecks that can undermine material strategies if not backed by resources and sound governance.

It is therefore important to develop a sustainability roadmap with clear objectives integrated into the value-creation plan, sequencing initiatives by ROI, feasibility, and risk reduction, so as to compound benefits over multi-year horizons where effects become more detectable.

Why it matters for investors and board members

If we believe that focusing on material issues is associated with superior performance relative to peers, then we must emphasize disciplined selection and measurement for value creation. Companies with integrated sustainability practices outperform comparable peers in long-term market and accounting results, consistent with capabilities, process discipline, and governance that reduce risk and enable innovation. It is therefore key to focus on:

- Selection discipline and materiality: boards must require ESG initiatives to focus on issues that are financially material for the business, applying prioritization methodologies based on economic impact, risk, and opportunity. This prevents resource dispersion and strengthens the value-creation narrative.

- Governance and accountability: integrating sustainability into the board agenda means defining explicit responsibilities within committees, overseeing financial KPIs associated with ESG, and linking executive incentives to material and measurable outcomes.

- Time horizon and resilience: relevant ESG metrics tend to deploy their impact over multi-year horizons. Boards must balance short-term demands with a vision of future resilience and competitiveness, communicating to the market the logic of long-term value.

- Strategic transparency: in an environment of regulatory and market scrutiny, boards must ensure that sustainability communication is truthful, consistent, and focused on value creation, avoiding greenwashing and strengthening investor trust.

In such turbulent times, it is important to demonstrate that the initiatives pursued have a clear strategic alignment and aim to create value for shareholders and other stakeholders. Sustainability must not remain a mere reporting or regulatory-compliance exercise.