Navigating an uncertain world: Building blocks for 2033 scenarios

EsadeGeo Working Paper | October 2020

Authors: Enrique Rueda, Angel Saz-Carranza & Tirso Virgós (EsadeGeo)

Content at a glance

- Introduction

- Essential uncertainties as drivers of change

- 12 uncertainties as building blocks for scenarios

Introduction

The major geo-economic transformation and re-shaping of global markets that has taken place over the last two decades is usually summarised as a process of globalisation and convergence. They are usually characterised by economic indicators: trade volume increases outpacing GDP; and faster growth in emerging market economies than in advanced ones. Digital technology has been a key enabler of globalisation—alongside steady (until recently) reductions in cross-border barriers.

The world is at a crossroads: widespread citizen dissatisfaction shakes up the politics of many countries and of international relations as the economic value generated by globalisation has not been shared inclusively enough—and the 2020 pandemic has made inequality worse in many countries; conventional trade in goods and services is stalling while the intangible component of the world economy grows; financial stability concerns resurface as actions to tackle the 2020 pandemic have resulted in major increases in sovereign debt; ... and more.

A lot can change in 10-15 years— we need only look back at 2005 to see that.

Scenarios are a valuable tool to navigate the resulting uncertainty and turn it into a source of opportunity for success. Scenarios, however, are not just a bundle of potential developments. It is the intersection of various dynamics that can result in powerful changes ... what in retrospect may appear to be inevitable surprises.

Our scenarios will look at how different socio-economic and political dynamics could play out over the next dozen years and how they would reshape markets and other aspects of the context for business by 2033. The first step towards building the scenarios involves identifying premises and the essential uncertainties that could drive change.

Essential uncertainties as drivers of change

Two types of change drivers will shape socio-economic dynamics and the future of markets and business. The essential uncertainties of the first type are in some sense also premises: they have some predictable elements – at least directionally – while also raising major questions about their role in the future.

There are three uncertainties of this type worth keeping in mind for our purposes.

- Demographics. Nothing much is certain—beyond a few basic demographic facts: we pretty much know how many people will be of working age by 2033—they have all been born and survived infanthood already. Population projections are more reliable than most other projections (certainly more reliable than economic or market forecasts). They show that we are living in a world of increasing demographic polarisation: many countries, including some with large populations in Africa and Asia like Ethiopia or Indonesia, still have "pyramids" – meaning young populations – while many others, mostly high-income countries have very top-heavy, ageing demographic profiles. How is this unprecedented imbalance going to play out, including in terms of migration flows? Where will all these new additions to the potential labour force between now and 2033 be living and working – if at all employed?

- Digitalisation. Although the pace may be uncertain, the impact of digital technologies is bound to continue growing – both in breadth and depth – with major questions over the accumulation of market power in the hands of a few players and on how the expansion of the "intangible economy" built on digital platforms will feature in policy decisions as footloose intangible links in value chains to capture increasing shares of the total worth of their output. Artificial intelligence and machine learning are bound to change the labour market and how businesses, governments and consumers relate to each other and will be part – to an unknown extent – of this process.

But there is also much digital polarisation: in 30+ countries at least 80% of the population uses the internet, while in 50+ countries where less than 20% do. The combination of digitalisation and demographic polarisation means that we face digital divides between generations that are a one-time phenomenon. Even in countries where the pervasiveness of internet access has reduced the digital gap between generations, we still we see very different attitudes to technology by "digital natives" (roughly people born in/after the 1990s) and earlier generations. Imagine what that difference is likely to be in countries with low current internet usage, and huge emerging digital generational gaps. - Climate change. The signs and some impacts are visible already and while the greatest concern is with longer-term impact, by 2033 it will be clear whether action to avoid catastrophic consequences has been adopted or procrastination and denial have prevailed—to our peril.

With these three factors prominently in the background, we focus on essential uncertainties that are even less predictable to anchor and guide our exploration of alternative paths for the world in 2033 and serve as building blocks for the scenarios, which will delve into the possible outcomes from intersecting uncertainties.

The list of uncertainties is not meant to be a comprehensive list of global issues but to spotlight the factors that will mostly shape economic and market dynamics and socio-economic outcomes over the next dozen years. One-off events (like a major terrorist attack, volcano explosion, etc.) and a possible new or resurgent pandemic are not considered. They would overwhelm the rest of the analysis and, in any case, deserve separate attention.

A few important factors with broad implications for the long-term future of the world are not explicitly included in this analysis to avoid "boiling the ocean" and keep the exploration manageable. The most prominent example is the longer-term effects of climate change – including rising temperatures and water levels – although attitudes in this regard are included among the essential uncertainties. Other such factors relate to the availability of natural resources (water, fossil fuels, minerals, etc.).

Exploring essential uncertainties implies looking inasmuch as possible for root causes or drivers of change

Exploring the essential uncertainties implies looking inasmuch as possible for root causes or drivers of change. While these will be unavoidably intertwined it is useful to attempt to isolate uncertainties and spotlight the range of plausible outcomes for each.

Because of the focus on root causes, most of the economic and institutional outcomes that create an important context for business are best treated as features distinguishing the different scenarios. The economic outcomes include economic growth momentum (including productivity trends and GDP plus the intangible), shifts in the geo-location of the engines of global growth, and trade, capital and people flows. Similarly, with institutional evolution and policies.

Below we present a set of 12 essential uncertainties. Each is characterised by a single-word indication of the endpoints defining the range of plausible 2033 outcomes and brief notes with relevant background are also provided.

12 uncertainties as building blocks for scenarios - and how they could be played out by 2033

1. Intergovernmental dynamics

How will have the relationships between different nation states changed by 2033? Are they tense and confrontational – on edge – or do they rely platforms for dialogue, cooperation and settlement of disputes in a general atmosphere of trust?

Recently, given factors such as the rise of China, the progressive withdrawal of the US from its role as global watchdog, and the West’s economic and political crises, there has been a perception of a more diverse global environment, far away from the convergence towards a liberal democratic "end of history" utopia. Questions about the ability of the international community to cooperate and engage in concerted action, as well as of the future of this "diversity" will be a key factor shaping international relations through 2033.

Among the many manifestations of divergence, the "Washington Consensus" has cracked along many lines, with countries across the world, including the Global North, contesting the effectiveness and legitimacy of its institutions. For instance, the IMF has been subjected to harsh criticism, arguing that their economic policy suggestions have been damaging for the economy of many countries.

While the old world order is till dying, the risks of political conflict, as well as the associated social and economic stability, are higher

Consequently, alternative arrangements and frameworks, as well as more regionalised institutions, have seen their role enhanced in comparison to other organisms. Even those which remained "global" and concerned with problems that transcended national borders (such as the WHO) have been subject to criticism and have been undermined by the actions of some major country governments (notably the Trump administration).

However, these dynamics threaten to destabilise the system built throughout the last 75 years, after World War II ended. In the valley of transition between one governance framework to another, there are possibilities for more confrontational international relations, and a progressive distancing of countries which were not allies but remained reluctant to engage more aggressively in their relations. So, while the old world order is still dying and there is no clarity on if and how a new one would (or if there will actually be a new one) the risks of political conflict, as well as the associated social and economic stability, are higher.

Consequently, we envisage a scale which ranges from confrontational relationship amongst states to a more constructive engagement, with global institutions that are perceived as legitimate by all international actors put – or restored – in place.

The first of these extremes is a world where relationships amongst governments move from merely bitter and tense to openly confrontational. Although wars are not common, there are multiple sanctions and attempts to destabilise rivals, either through cyberattacks or other means, such as raising tariffs or imposing sanctions. Without legitimate global institutions, it is difficult to hold aggressors accountable, and countries retort to a more retributive foreign policy.

In this extreme, global institutions become progressively a relic from other era

However, in this extreme, while global institutions become progressively a relic from other era, new regional agreements take their place. "Closer to the ground" regulation allows for more innovation, and a patchwork of alliances is crafted amongst states with closer economic, cultural or geographical ties.

At the other end of the spectrum, there are fluid relationships amongst states. In order to establish new basis for cooperation, there is an attempt to create new institutions, or reform those of old, to make them legitimate in the eyes of all participants of the international sphere, and not a selected few. With their powers increased, these organisations set principles and norms regarding trade, AI, or climate change, contributing to an atmosphere of stability and trust in which different interests are attempted to be balanced transparently.

2. Super-power dynamics

This axis of uncertainty is concerned with the evolution of the relative strength of the main power blocs, as well as the relationships among them. We seem to be at the end of a largely unipolar era, but it is far from clear what will be next: a bipolar era; a multipolar one; or a more fluid nexus of relationships.

After the end of the Cold War, and of the US-USSR rivalry, there was a clear consensus on the position of the United States as a global hegemon, main superpower, and "police" of a liberal world order. However, that predominance has been put into question in the last decade, with the forceful rise of China, the broader shift of the economic centre of gravity towards Asia, the re-assertiveness of Russia, and the presence of a powerful regulatory power in the EU.

At the same time, the US has withdrawn from certain commitments on the international sphere, especially (but not only) during the current administration. A more detached stance of the former global watchdog, combined with an increase in the relative strength of the main rival, in the context of more integrated markets and the spread of digital technologies, have increased the range of tools deployed by superpowers and made the use of soft power even more important than before. Although there are still a lot of military conflicts, many disputes take place in areas such as regulations, taxes, sanctions, and foreign investments. Initiatives such as the Chinese BRI or the push of the EU to set global rules are a testimony to this.

Although there are still a lot of military conflicts, many disputes take place in areas such as regulations, taxes, sanctions, and foreign investments

The combination of these factors poses important questions for the future of the international system. The rise of one power, along with the decline of another, creates the conditions for increasing the risk of a confrontation that transcends the verbal domain. With the development of new technologies, as well as a growing interdependence between countries, we might see a weaponisation of the latter, and weaker states being trapped in a network of threats and precarious alliances within the sphere of influence of one of the power blocs.

Is a more multipolar world, with multiple decision-making centres and a lack of an all-encompassing ideology, or even a common framework of legitimation of interventions and actions, taking shape? Or is this just a transition phase? The economic interdependence has not developed on par with stronger diplomatic and politic ties amongst power blocs, and thus the possibility of an overlapping consensus has become more and more remote.

The US has been drifting away from traditional allies, such as the European Union, and from its former commitment to multilateralism, as well as to global institutions or previous arrangements with allies (such as NATO), but is this reflecting a passing mood or a more fundamental change? On the other hand, China’s apparently inconsistent political and economic models and its growing global ambition (One Road/One Belt, etc.) seems to have caught much of the Western world by surprise and its sustainability is not obvious.

China's growing global ambition has caught much of the Western world by surprise and its sustainability is not obvious

Finally, the EU struggles to find consensus to deepen its integration, and acts a sort of regulatory power, with a changing relationship with the US and tense dealings with China, which is increasing its presence in its eastern countries and borders.

The present situation is open for developments in very different directions. From a retooling of relationships amongst power blocs, resulting in a multipolar but peaceful world, where this multipolarity is seen as an asset, to a straining of these contacts, and a progressive decoupling and disconnection that derives in survivalism and more tense international relations.

We have presented this uncertainty as a continuum that moves from a "split world" to a nexus. The former extreme is that of bipolarity, with a confrontational relationship. Here, all other countries would stand between revamped spheres of influence, with very few finding room to stand aside as non-aligned. Supply chains would be changed with both blocs trying to keep their production and resources closer to home and reduce as much contact as possible with their rival, except for confrontational actions. Trade wars or proxy conflicts could see their numbers increased in this extreme and international agreements become very elusive—no matter their potential value.

In the other extreme, there is a multipolar world, where no superpower has dominance. This fluid balance of powers creates an environment more propitious to international agreements, although not all of them with "win-win" potential. It also helps in consolidating new governing principles and common sets of norms for international organisations, creating nexus of relationships in a more multilateral setting. This trend continues, and the world sees multilateral agreements as the way forward.

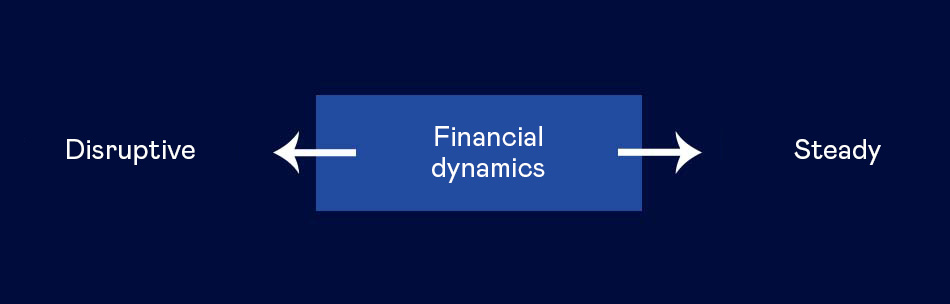

3. Financial dynamics

How will financial markets evolve throughout the decade? Will they remain stable, with incumbent players remaining largely dominant, global institutions in place and low interest rates? Or will fintech developments, crypto-currencies, inflation, and exogenous crises result in greater disruption and instability?

The pandemic crisis of 2020 has had a significant impact on financial markets—notably increasing the volatility of securities markets. However, this exogenous impact could be seen as mainly increasing the level of uncertainty around financial dynamics. This uncertainty can be explored through four fronts.

- First, on the global regulatory front could we see agreements such as Basel III consolidated, alongside cooperation among national financial regulators, or side-tracked—reflecting divergent views on regulation and financial controls. Similarly, could international institutions like IMF and BIS become stronger and well-supported or could there be little global coordination and a greater role for regional institutions (in the EU, Asia...).

- Second, will ample liquidity and low interest rates continue, or will the large monetary interventions and sovereign debt issuance around the world result in a burst of inflation and spike in interest rates. Intermediation dynamics are also worth keeping in sight. On one hand, there is the role of financial hubs—will existing ones consolidate and result in the gap between the major ones (New York, London, Tokyo) and alternative ones grow; or will there be a dispersion with budding financial hubs (Singapore, Dubai, ...) growing larger and new ones emerging. To compound the uncertainty, are the unprecedentedly large corporate cash piles that could be moved around swiftly.

- Third, fintech and the convergence of ecommerce and finance could rapidly alter the structure of the market and even challenge current regulatory boundaries. Use of big data, adoption of new AI-based solutions and flexible approaches could break the dominance of established actors, opening the doors to more competition. Predominant digital platform corporations could use their financial muscle, consumer reach and technological prowess to present powerful alternatives to traditional banks, insurance companies and other financial incumbents.

- Fourth, is the world of currencies going to remain largely unchanged or will digital currencies, cryptocurrencies, a different approach to reserve management and international payment mechanisms upset the role of exchange rates? Two possible extreme outcomes serve to characterise this uncertainty. One of them is that the period through 2033 has been characterised by disruption along the four fronts: global financial institutions lose support and the capability to prevent and intervene in crises; a jump in interest rates and a disaggregation of financial hubs; major share of financial services being provided by firms that were originally not financial; and the spread of cryptocurrencies.

On the other extreme, we can envision a stable environment including a steady financial dynamics: Basel-type regulatory frameworks become consolidated for banks and expand to other financial institutions while the IMF is given enough firepower to face crises; interest rates remain subdued; incumbent financial institutions retain major shares of financial services (including through fintech acquisitions and regulatory protection); and cryptocurrencies remain a fanciful notion with limited niche reality.

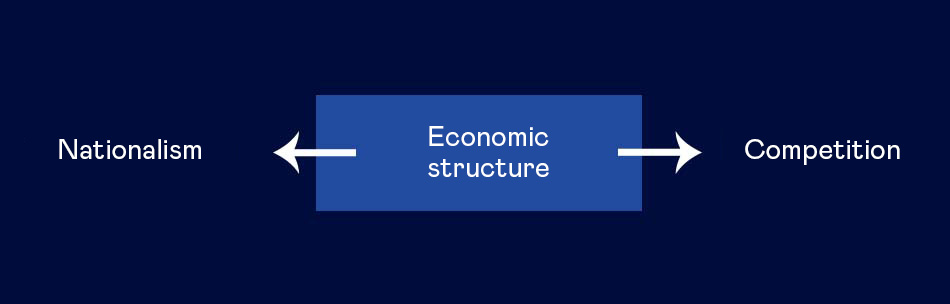

4. Economic structure

This axis of uncertainty is concerned with the role of the state in the economic life of countries. Will recent events result by 2033 in the state taking greater stakes in economic assets and a more assertive role in markets and transactions or will they represent a temporary phenomenon with a retreat starting by the mid-2020s?

Throughout the last 40 years, there has been a certain retrenchment of public spending and state functions, with the overarching idea of freer markets and private enterprises being more effective than publicly owned enterprises and interventions. However, given recent financial crises and events such as the Covid-19 pandemic, policy steps have been taken in many countries tantamount to an increased role of the state. At the same time, protectionism that had been in retreat for over two decades has returned in recent years.

Recent crises and natural catastrophes have put the spotlight on strategic vulnerabilities and lack of resilience that had resulted from the search for efficiency via highly fragmented global supply chains. Slogans such as "America first" or "Made in China" are manifestations of this, combined with actions such as the retreat from multilateral treaties, perceived as "harmful" for the country and its workers, or increases in tariffs for foreign imports.

Globalisation and free markets are no longer seen as the most direct way forward towards wealth

In fact, data from the WTO shows that in the last 12 years, members of the organisation have introduced almost 2000 trade-restrictive measures. This numbers rose especially in the period 2018-2019, which was the year with the historically highest level of trade-restrictive measures. Countries such as the US, formerly champions of the free trade-based world order, have been amongst the harbingers of this changing dynamic. A contributing factor has been the perceived stagnation of the economic situation of Western middle classes in the last decades, while middle classes in developing countries have continued their economic growth. Globalisation and free markets are no longer seen as the most direct way forward towards wealth.

In this context there has been a tendency towards strengthening potential national champions, protected, or even sponsored by the state, not only to improve current capabilities but also to compete in the possible tech and trade races to come. Fears of hostile take-overs or of businesses with foreign capital that would not be aligned with national interests in the event of a political, economic or military conflict, have reinforced the notion of "strategic control" of key assets of the economy. The implications of this axis of uncertainty are, thus, far-reaching and set to have meaningful changes, as it affects the very essence of the political economy of nation states.

We identify two possible avenues towards which this uncertainty could develop.

- On the one hand, a rise of economic nationalism and protectionism, not only confined to certain nations, but extended throughout the globe.

- On the other, an updating of the rules of competition, a renewed faith in free markets and a series of regulations to put in place fairer norms in access to certain markets.

The extreme of nationalism presents a world where states have taken the decision to expand their role in the economy to an unimaginable extent in the latest decades. Through the re-acquisition of key business in strategic sectors and a limitation of foreign direct investment, they would seek to limit the chances of external actors messing with the political economy of the country, as well as creating local supply chains to answer against new threats. At the same time, through the promotion of national champions, countries would try to break those very same barriers to foreign investment in other countries.

On the opposite extreme, a world focused on interstate competition is one where countries have reached an agreement about the problems of the dominant model in the last years, while at the same time stayed away from the lure of protectionism. By providing new sets of rules for fair competition, avoiding abuses of power, and fighting against excessive concentration of business, they try to generate a level-playing field for actors, as well as to ensure the efficiency of free markets. This extreme sees a renewed faith in the workings of the current system, although with new regulations to face the new challenges of the century.

In between these extremes, states can attempt to strike a balance between protectionist measures in certain areas and a more competitive outlook in other sectors. These decisions should be heavily influenced by actions taken by other states, in a sort of diffusion effect that would change perspectives both within and between blocs.

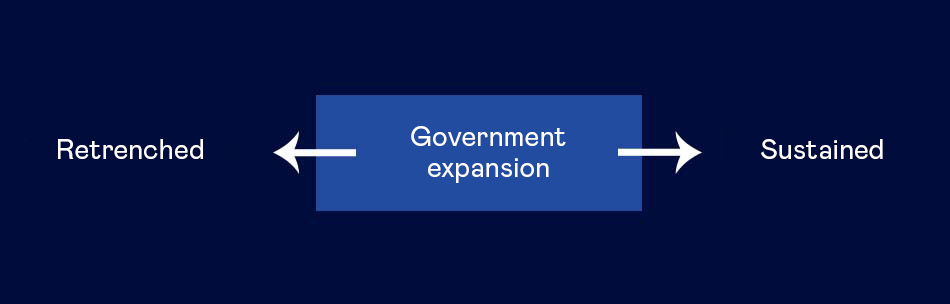

5. Government expansion

Have recent crises, which gave states expanded intervention powers and expenditure margins, led to a permanent increase of their political and fiscal powers? Or have concerns about the size of government, its intromissions in the private sphere and the deficit levels resulted in a retrenchment of its capabilities?

Both the financial crisis of 2008 and the Covid-19 pandemic of 2020 brought back to the political conversation ideas about a bigger role of the state in the economy.

Discussions about the need for more fiscal pressure, as well as the possible nationalisation of key sectors are not out of the public sphere now. Conversely, fears about this increased role of the state and actors such as those worried with possible invasions of the private spheres or sub-national governments with reduced political powers, have also sparked the idea of keeping the powers of the state confined.

Governments, as it stands now, have deployed in the last year a level of activity that was almost unprecedented in the last 40 years.

Governments have deployed a level of activity that was almost unprecedented in the last 40 years

By getting involved on key areas of the economy, investing vast amounts of money in protecting citizens from the virus and the economic impact of the measures to contain it, and setting unprecedented restrictions in daily life, the scope of the state has been increased throughout the crisis, re-igniting the debate between proposals for less activity of the state, in order to allow for freer market, and stances in favour of an expansion of state powers to draw the reins of the economy. These two perspectives also clash alongside a series of cleavages, such as the powers vested in national and subnational governments or the checks-and-balances in place to control the action of the state when interacting with citizens.

Arguably, it was not only the Covid-19 and the financial crisis of 2008 what propelled the expansion of state powers. There are some dynamics that have become more apparent in the last years. For instance, the progressive ageing of the population, especially in the West, resulting in increasing dependency ratios and the need for more social spending. At the same time, the rise of inequality, and a growing anger towards the perception of Western middle classes being in the losing end of all of the latest economic and political processes, have set the stage in many countries for the state to demand more resources, in the form of taxes, to address these problems.

Countries around the world have been forced to reinforce their roles as protectors of their citizens

Similarly, developing countries need to reinforce their capabilities, which leads them to look for more resources, and in the absence of growth through other sources (such as foreign investment), this expansion could be seen as a potential silver lining.

Countries around the world, no matter their political system, have also been forced to reinforce their roles as protectors of their citizens, and not mere vigilantes of the economy. This increase in the powers of the state has been demanded by citizens in the last year to control the pandemic. Studies have shown that expansion of government is easier than taking back the powers that have been vested on it.

However, in the case of mishandling of the crisis, as well as of the urgency powers given to governments, there could be pressure for reducing the size of the state and shifting the roles of different levels of government back to 2019 levels, or even further.

Corruption can be another factor. Research has shown that in times of crisis, especially when lives are at risk, the threshold of toleration with corruption is reduced for citizens. Corruption involving money that should be destined to heal the wounds of the crisis could prove fatal for the prospects of keeping the expanded powers in place. Mobilised civil society can demand "sunset clauses" of termination of the exceptional powers of governments, if they were not already in place, ensuring, if not retrenchment, at least the continuation of the "status quo".

In times of crisis, especially when lives are at risk, the threshold of toleration with corruption is reduced for citizens

Finally, it must be noted that the increase in public debt that the pandemic emergency has required could also prove a strong force for a retreat to small government.

We envision two extremes of resolution of this uncertainty.

- On the one hand, a sustained expansion of governments, maintaining the powers vested on them throughout the crisis and even increasing them. An effective handling of the pandemic, as well as of future challenges, coupled with the state capabilities to effectively deal with them, could provoke a strong current of public opinion in favour of sustaining the measures. Greater support for protection "from cradle to grave" would emerge, with governments taking a bigger role in the life of citizens, including intrusions in the private sphere, which could be perceived as legitimate insofar as they contribute to a higher level of security in all aspects.

- On the other, a retrenchment of the powers of the government, and a strong current of opinion, including because of fiscal discipline or reluctance by citizens and businesses to accept more taxes, in favour of keeping them in check. Mishandling of emergency powers, power struggles between different government levels, corruption in economic policies, lack of state capability to protect citizens or warnings about the loss of privacy of citizens against more vigilant states. Many factors can contribute to shows of dissatisfaction with powers that were a temporary measure for an exceptional situation to be maintained.

6. Domestic powers

Has the impact of different exogenous crises affected the perception of the legitimacy and utility of traditionally centralised nation states? Has poor management and demands for administrations that are closer to the citizens tilted the balance in favour of more decentralisation? Have cities strengthened their position in the international sphere as a result of these dynamics and are posed to have a stronger international role by 2033?

Classic diplomacy has been centred around the pre-eminence of nation states. The Westphalian model, present since 1648, has given them the central role in handling politics, economies, and relationships with other actors. Processes of decentralisation, either by bringing together formerly separate states, or "holding together" unions that required federalisation, had not disputed this pre-eminency. However, on the wake of globalisation, cities have come to dispute this notion.

It is obvious that cities have been actors of their own for the most part of history. As hotspots of economic growth and innovation, connecting citizens from different backgrounds and acting as agglomerates of businesses and talents, they were a linchpin of the progress of countries, as well as a source of rights and freedoms for citizens. In modern times, they have also been harbingers of processes of even more concentration of population and have gained a certain amount of relevance in international talks.

For instance, Chicago and Mexico City stroke a trade agreement in 2013, without considering the desires or global strategies of their federal states. Similarly, mayors of cities such as Los Angeles, Paris or Barcelona have gathered to reinforce their commitments to fight against climate change. And, throughout the crisis of the Covid-19, mayors were often seen as the first line of defence against the expansion of the virus, acting as protectors of their citizens, contact with civil society and providers of resources.

Cities are rising as global actors of their own and becoming the sources of social integration

This, in turn, could lead to a change in the perception that citizens have of the state. While still the legitimate entity that controls a territory through the use of power, their handling of recent crises, compared to that of mayors of the most relevant cities in that territory, can have an impact on the perpetuation of that legitimacy. With cities rising as global actors of their own, and possible future crisis eroding even more the perceptions of competent management by the state, the parameters of political interaction both within and across borders could change significantly. With cities becoming the sources of social integration, and providing stronger bonds of shared identities, they could dispute citizens’ allegiances with states.

However, it must be noted that these actions by cities in the international sphere are still sparse. For the most part, mayors solve day-to-day problems and lack the resources to combat bigger scale threats, such as pandemics, relying instead in their communicative power to demand more from the state. Declarations, joint statements, and media presence during crises do not amount to political power. Cities are still not sitting in the main circles of power, for instance, representation in international organisations.

Communicative power is important, but political power is more. Without "devolution" processes of competences from the state, the former could not turn into the later. We identify a continuum of possible outcomes, with a more centralised power on the one extreme and dispersed nods of power, usually placed in great metropolis, on the other. The former presents an evolution where the states can effectively handle present and future crises, gaining the trust of citizens to maintain their status.

Failures in processes of decentralisation provoke a recovery of certain functions by strong central states

At the same time, failures in processes of decentralisation, either by mishandlings of relevant issues or by incorrect attributions of competences, provoke a recovery of certain functions by strong central states, re-stating their pre-eminency and crafting a new Westphalian world. Despite the strong media presence of some mayors, and the economic power that cities still hold, nation states remain as the source of political power and allegiance of citizens.

On the other extreme we find that trust of the citizens has been placed in the administrations which are closer to them. Given claims for administrations which are "closer" to the citizens and knowledgeable about day-to-day problems, greater legitimacy is bestowed upon cities, which become stronger vis-à-vis the state. In this outcome, more competences are given to mayors, becoming much more than intermediaries, and taking the responsibility to generate, tax and allocate resources, transforming big cities into a new form of "Polis".

Social capital and networks of civil society play an important role in this change, aiming for more direct democracy and grassroots connections to governments. While regions also gain from these "devolution" of political and administrative competences, cities are the major beneficiaries of their stronger connection to citizens.

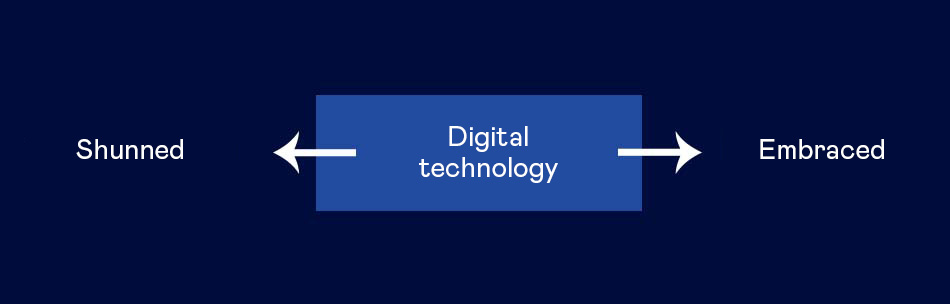

7. Digital technology

Are new technologies, such as artificial intelligence (AI), machine learning or AR/VR, on the way to become central to the relations between businesses (b2b), from businesses to clients (b2c) and from citizen to citizen (c2c)? Are they changing, and will continue to do so, the consumer experience, supply relationships and the labour market? Or are they stalling, amongst fears of cyberattacks, technology fatigue and luddism?

Behind the use of technology at any given point in time there are two factors:

- innovation, based on new developments, usually by scientific teams and driven by experimentation;

- and adoption of existing technological possibilities in workplaces, supply chains, consumer experience and other areas of business.

In the medium terms, the narrowing of this gap between availability and adoption of technology can have the greatest impact.

Given the surge of new technology development in recent years, it is how this availability-adoption gap evolves over the next decade that will determine the role that technology plays by 2033. AI exemplifies this uncertainty: with many studies pointing to its disruptive – and productive – potential; and a long track record of disappointment and delayed adoption.

A major question mark is about scalability. For large corporations it is easier to invest resources in implementing AI across different parts of the value chain, and in almost all sectors. However, for SMEs, that same process can be costly, resulting in "divesting" resources instead of "investing it". A recent survey by IBM showed that while almost 50% of large companies in the world were adopting AI, only around 30% of SMEs were doing the same.

AI and other digital technologies raise concerns in the minds of many citizens

In addition, AI and other digital technologies raise concerns in the minds of many citizens, which could act as a demand dampener or regulatory hurdle to their adoption. Words such as those of Elon Musk, regarding the dangers of AI, or Vladimir Putin ("whoever controls AI will control the world") can only serve to increase the fears of a future where "broad AIs" can control every aspect of human life.

Also, once a corporation or state becomes a leader in technological terms their "first mover" advantage could become the source of quasi-monopoly power and they could play an asymmetrical role reshaping markets and competitive positions, in all kinds of sectors.

Following these dynamics, we have identified two possible outcomes, which sit at opposite extremes of the spectrum.

- Firstly, a world where digital technologies are embraced by business, governments, and citizens, enhancing their confidence in the possibilities of AI and other new technologies. By providing an adequate institutional context for innovation and adoption of AI in SMEs, as well as adding digital skills to educational curricula, governments ensure that citizens can understand its advantages. This, along with more coordinated action in favour of transparency in AI, helps in promoting more adoption of digital technologies by businesses for their relationships with other businesses and clients. In time, even citizens adopt these new technologies as platforms for their relationships with governments and other citizens, facilitating the organisation of grassroots movements.

- On the other hand, we envision a world where the population shuns away from digital technologies, in a sort of new Luddism provoked by not just fear but also perverse experiences with the "black box" decision processes of machines, as well as the threats to human jobs. Problems of scalability widen the gap between large companies and SMEs, increasing inequality both within and across nations, and development of new technologies is slowed down due to the lack of enough productivity gains from new digital technologies, as its adoption is exclusive of very few concentrated big actors. Given this, corporations and states end up treating these technologies mainly defensively while looking for other ways to gain a competitive edge over rivals.

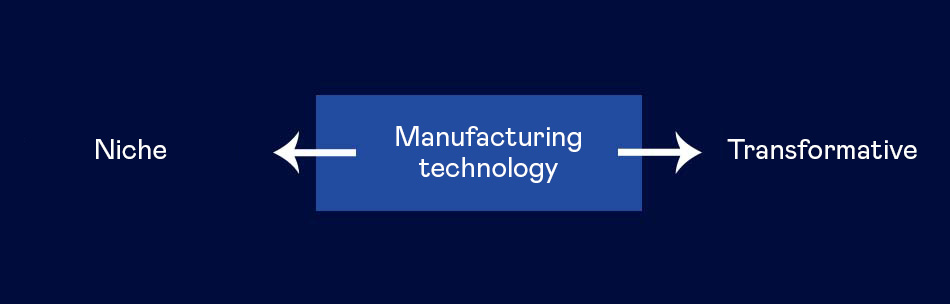

8. Manufacturing technologies

By 2033, has manufacturing technology remained largely unchanged, with significant change confined to a few sub-sectors and places? Or have automation technologies such as robotics, and applications of AI and IoT resulted in sweeping changes, including in sectors that seemed less prone to it? How much, how fast smart manufacturing spreads will have major implications for the composition of labour markets and for the skills in demand.

The potential for robots and other aspects of "smart" manufacturing is enormous given that the relevant technologies are largely available already (more than a million robots is estimated to be in place). Machines which can take on the most tedious and repetitive jobs can free up time for other workers to focus on more complex tasks, while the feeding of data to AI and expansion of the Internet of Things could lead to interconnected factories, with a constant flow of data and alerts regarding the status of machines, possible bottlenecks in the productive process and in supply chains or potential harm to human workers.

The potential for robots and 'smart' manufacturing is enormous given that the relevant technologies are largely available already

The launch in 2015 of the "Made in China 2025" project was part of an ambitious plan to turn China into the most advanced and innovative economy in the world, signalling a decision to invest heavily in technologies with the potential to turn what was considered as an activity relying on blue-collar workers (and low wages) into a new source of competitiveness.

However, there are counters to this. The hurdles to adoption of "smart" manufacturing technologies and IoT that have been in place for some time – accounting for disappointments and even a dismal failure of some past predictions – could well prove persistent. In addition, 75% of those 2 million robots are concentrated in 5 economies (China, Japan, South Korea, the US, and Germany) and almost specifically in the automotive. This concentration can widen the gap with other states, increasing global inequality and with the possibility of the formation of international alliances to avoid diffusion effects of technology.

In the light of these dynamics, we envision two extremes in the spectrum of possibilities for how this uncertainty could be resolved by 2033.

- At one end of the continuum we envisage these technologies spreading slowly and mostly through niches: some corporations, countries and subsector which largely remain the exception and very gradually only extending beyond that. The hurdles of relative cost (especially for SMEs), complexity and reliability are augmented by regulatory actions reflecting voter and union pressure to block the replacement of human labour by machines. Overall suspicion of IoT in both personal lives and factories has increased and also blocked much progress in that regard, including through concern of IoT serving as a possible Trojan horse or black box that increases the power of a small number of white collar workers against the larger numbers who work manually. Smart manufacturing remains something closer to science fiction that everyday reality.

- At the other end of continuum of possible outcomes by 2033, there is a situation in which these technologies have spread widely and played a transformative role, making their sectors more efficient and productive and, either, imitated by other sectors across states or providing huge competitive advantage to those who have led the adoption of smart manufacturing. As adoption of robotics spreads, a kind of Moore’s Law is unleashed which results in rapidly dropping costs of reliable robots and creates the opportunity to SMEs and playing in a more level field. Similarly, countries that focused early on creating the conditions for smart manufacturing to thrive reap rewards—especially if they have managed the transition by fostering the deployment of technologies that work as "co-operators" and not mere replacement for humans. Grievances about job losses remain, however, and the process of transition for some workers, and states, becomes dire.

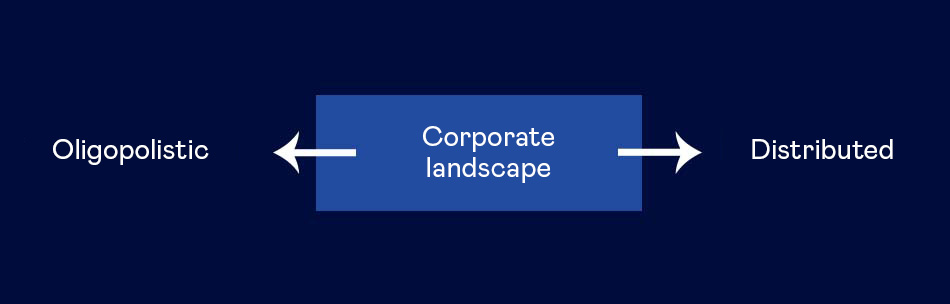

9. Corporate landscape

By 2033, have market structures evolved to consolidate the concentration of economic power in the hands of a small group of corporations, effectively creating oligopolies—mainly driven by the expansion of the market and financial power of digital empires? Or have anti-trust and similar policies to assert the control of the state led to break-ups and other constraints on the expansion of digital mega-corporations resulting in more dispersed markets?

Following the rapid growth of digital and "platform" companies, their market and financial power has expanded to unprecedented levels: the market capitalisation of just seven companies (five from the US and two from China) represents close to 10% of global market capitalisation. These companies have been harbingers of innovation and changed many aspects of everyday life—for individuals and business alike. Dynamics such as the migration to the "cloud" and AI applications fed by the massive data stored there has the potential to accelerate such concentration.

By 2033, the market capitalisation of just seven companies represents close to 10% of global market capitalisation

In another indication, half of the contracts of the Department of Defence of the US have been allocated to the same 5 companies, and companies such as Google or Amazon have spoken about their key role in the AI race or the protection of national security.

There is, however, concern with the stifling of innovation that these companies could be ensuring with their dominance of the corporate landscape. By "consolidating" themselves, they effectively absorb promptly or preclude competitors, which could be more innovative and dynamic, as well as becoming part of a more diverse landscape. At the same time, by being too big to fail, or to be broken and having such a strong economic power, they also can have the ability to hold their HQ country hostage of their demands under threat of migrating.

Digitalisation and globalisation have been also forces working in the background of this expansion, allowing these corporate empires to move into the realm of internet and less regulated areas, co-opting markets that were out of reach for previous big corporations. In the international sphere, by effectively transcending national borders, and barring strong global regulations, they can avoid being kept in check for their activities and projects. All these concerns could well create impetus for policy and regulatory intervention to change the dynamics of consolidation.

Thus, we envision two possible extremes in the continuum of possibilities.

- One of them is a further consolidation as corporate digital empires keep snowballing and absorb or derail possible competitors and alternatives while asserting their vital role across a series of key markets in different states. This situation would imply that virtually all companies (large and small) would have to become part of their ecosystems, and many states would end up being dependant on a small number of corporations for their technological future.

- The other extreme is a backlash driven both by citizen concerns over these huge "big brothers" and by state concerns over control. The result would be strong anti-trust laws and a series of global norms (including on taxation) and international agreements that force break-ups, spin-off, divestitures and limit the scope of activity (for instance financial services) of the large digital corporations. Through distribution of power across other emerging corporations and ensuring a level playing field, competition could be re-sparked. Citizens, at the same time, would see an increased diversity of options in their digital activities.

10. Privacy protection

By 2033, have citizens adopted protective measures against the extended use of their data by companies and governments? Have the later also pushed for forms of data flow controls, opt-in and other forms of privacy protection? Or have all actors adopted a laissez-faire approach to this topic, given the convenience of connectivity, customisation, and personalised choice?

The growing interconnectivity of the world has brought forward a wide array of services and options for consumers across the planet. With a simple click, any individual or business can access a vast network of information, providers, offers and personally targeted content that was unthinkable two decades ago and uncommon even a decade ago.

Each of these clicks, however, creates patterns of preferences which pass through algorithms to offer an even more personalised experience to the user. The associated trade-off is clear: you are giving away personal data of your habits, preferences, location, etc.; in exchange for a better information experience, more comfortability when surfing the net and greater convenience in commercial transactions.

The growing interconnectivity of the world has brought forward a wide array of services and options for consumers across the planet

Part of the uncertainty is related to whether the combination of connectivity and artificial intelligence is going to amount to a general-purpose technology having a similar impact to previous ones, like electricity, and with data becoming its main fuel. By feeding computers with it, they can learn through processes of deep or machine learning, improving their performance and offering better services.

In the last years, there have been efforts to regulate the use of personal data on the internet. For instance, the European Union approved the General Data Protection Regulation (GDPR) in 2018 to set a common normative of use of personal data for business operating in the EU. This regulation, with its advantages and flaws, has been heralded as a model of success, inspiring legislation in places such as California or Australia, and is in line with the growing preoccupation with the possible misuses of data. Will it become the norm or the exception globally?

The Covid-19 pandemic has also brought to the front of public opinion the question of the trade-offs between privacy, and the protection of the personal sphere, and security.

Given the focus on testing and tracing, smartphone apps that could provide governments with information about who had been in contact with a positive of Covid-19 were branded as extremely useful in the fight against the pandemic. However, there has been a lot of debate on the merits of this online tracing when compared to the technical and ethical problems that poses the collection of data that goes beyond personal preferences: data about citizens’ health. Fears of becoming "pariahs" of falsely reported positives that force those in contact to lockdown and of the collection of that very personal data by governments (in a sort of "return of the Big Brother") have become normal during the process of development and implementation of these apps.

Consequently, we envision two possible extremes in the continuum of possibilities that this uncertainty presents.

- One possibility is that citizens effectively demand tighter protection of their personal sphere, using routinely every opt-out option provided and arguing against overly complicated terms and conditions or unclear rules that must be accepted to surf through the net. At the same time, they demand accountability and sunset clauses for the use of their data in situations of crisis, and norms such as the GDPR become a standard that transcends regional boundaries. Through global arrangements, either carefully crafted or acting as patchworks for future developments, there is a pushback against possible data colonialism, and the digital realm becomes more regulated than today.

- The contrary possibility is a situation of very lax forms of data protection. Either by the impact of an unexpected crisis or by the comfortability and convenience of receiving personal offers and services, citizens move away from more stringent requirements, and are happy to cede their personal information. Health-monitoring apps and carefully personalised services become the norm, and rules such as the GDPR or other forms of data protection become merely codes of "good practices" that are never institutionalised. Some countries engage in "data colonialism", as they use their superior cybernetic capabilities to extract data from citizens of other places. At the same time, big transnational businesses, with similar powers, also engage in these practices, rendering the self-determination of many countries irrelevant. But citizens feel that the infringements of their private and national spheres are worth the price in terms of their wellbeing—or are too hard to fight against.

11. Social dynamics

Has social dissatisfaction been effectively addressed by institutions, providing channels of participation and solutions to its causes? Or has it spread and become more "guerrilla-like", locally, nationally as well transcending national borders?

This axis of uncertainty is concerned with the evolution of forms of political action that go beyond traditional channels. More specifically, different forms of response to actual or perceived problems that demand changes across a wide range of policies or institutions, either on more liberal terms, or aiming for what has been defined as "Traditional, authoritarian and nationalist" (TAN) outlooks.

These expressions of social dissatisfaction have been especially present in the last decade, with economic crises and changes in labour markets and in the global economic structure damaging the prospect of enjoying a better life than their parents for younger generations.

On top of this collapse of expectations—or even opportunities, there has been a certain resurgence of the idea of the need for more direct channels of interaction with the government, as well as disputes of what has been perceived as a technocratic approach to politics. Social media has helped in providing platforms for connection that help in reducing the threshold for participation in demonstrations and other forms of contentious action. If parliaments and governments lose legitimacy, non-institutional action becomes more prevalent.

In democracies, alternative forms of political action are perceived as one of the only ways to achieve meaningful change

Given these dynamics, the streets become a source of "voice" for those who traditionally only had the opportunity to remain loyal to certain parties, regimes or governments, or to exit towards the abstention or exile. In democracies, the perceived lack of representation in the circles of power (either amongst political or economic elites) leads to alternative forms of political action being perceived as one of the only ways to achieve meaningful change.

Even in authoritarian contexts, the interaction of corruption, economic damage and tiredness with the regime can turn social dissatisfaction into protests in the street which could lead either to democratisation processes or to harsh repression.

Of course, these expressions of social dissatisfaction entail certain dangers. On the one hand, there is the possibility of minorities within the protesters co-opting movements for their own personal gain or for objectives which are not those of the protesting collective. It has been studied that well-organised minorities are very able to control social movements, and, consequently, stemming them towards their favourite outcomes and not the most efficient or normatively better ones.

On the other, there is the risk of the use of violence, given the lack of fulfilment of certain objectives. A group of politically active people constantly mobilised, who does not seem to achieve any of its goals can end up exploring new avenues of contentious politics, including the use of violence. Even if non-violent forms of protests are known to have a greater chance of success, utilitarian rationality is not always the guiding principle for movements stemming from passions.

We envision a continuum with two extremes on how this uncertainty could resolve itself by 2033.

- One would be a situation of guerrilla-type activity in the streets of many countries which generates instability. Social movements in this situation have decided that political action through formal institutional channels has proved inefficient to achieve their objectives, and coordinate across national borders to present challenges to both autocratic and democratic governments. Assemblies, demonstrations, and other forms of contentious politics become the norm, with the legitimacy of traditional channels completely eroded, as well as of traditional states, with growing mistrust amongst citizens. This also causes a backlash from governments and segments of the society which oppose these changes, furthering instability, and more affectively polarised societies, without common grounds for debate or commonly recognised institutions.

- On the other extreme, we see an "institutionalised" form of contentious politics, where institutions, such as government or political parties, have understood the virtues of accommodating certain demands, curtailing unrest and providing a more direct democratic experience to citizens. Social movements also understand that a calmer route, with peaceful actions and acknowledging the legitimacy of traditional actors, is a more efficient tactic that contributes to fulfilling their goals. Governments also open up new channels of participation, without losing sight of traditional artifacts of representation, such as voting. New methods of participation or democratic experiences could be tested to improve representation across multiple dimensions.

12. Climate action

Has perception of threat brought forward by the Covid-19 pandemic been a catalyser for a change of consumption habits, political opinions, and travel choices for citizens? Are they moving towards more environmental accountability of businesses? Or has the focus been placed on the short-term material consequences of crises, slowing down the efforts to tackle climate change?

In recent years, the issue of climate change has encountered conflicting currents. On one hand, 2019 was a year which had proved the political strength of the fight against climate change building on the 2015 Paris Agreement.

The spread of social movements as represented by Extinction Rebellion or Greta Thunberg served as a reminder of the support for green issues amongst young voters—as did the gains of Green parties in Germany and the proposed European Green Deal of the new EU Commission. On the other hand, in the United States, significant figures in the minority left wing of the Democratic party are arguing for a Green Deal, but the Trump administration formally backed out of the 2015 Agreement. And the question of burden sharing across countries has hindered progress in implementing the Agreement.

Corporations, NGOs, and citizens have also taken stances, with the latter demanding that the former play a greater role in fighting against climate change

However, the Covid-19 pandemic put a halt on all political activity not concerning the spread of the virus, the protection of the lives of citizens and the best ways to preserve the employment and the productive structures of economies on the verge of a possible collapse. The "Green issue", thus, already faced a conundrum compounded by this crisis. Confinements during the crisis have given a taste of alternative lifestyles, with reduced mobility and virtually no international travel, and this has given hope that the crisis will provide a boost to action on climate, avoiding disastrous climate change.

Corporations, NGOs, and citizens have also taken stances, with the latter demanding that the former play a greater role in fighting against climate change. Wildfires, floods or increases of temperatures could also play in favour of demands for a more urgent action against climate change.

The economic impact of the crisis could well result in a "putting money on the table now" attitude and worrying about fiscal constraints instead of focusing on the long-term future of the planet. Even before the crisis, initiatives such as a fuel tax sparked protests in countries like France, given that they had a more profound impact in the personal economies of blue-collar workers. Similarly, flight taxes could widen the affordability gap between income segments.

How this tension will be resolved will hinge to a large extent on the relative strength of constituencies defending their short-term economic interests (and scepticism, self-interested or not) relative to that of movements convinced of the importance of climate action to protect the legacy of the planet for future generations—and "walking the talk" to that effect in their personal choices.

The prospects of 'Green new deals' or 'green jobs' either fail to accomplish their goals or are erased in favour of policies which provide short-term results

How that dynamic plays across countries – especially the ones from which action will be most significant for climate change progress – will be decisive. Can actors such as social movements craft the fight against climate change as part of a "just transition" that will also be positive for blue-collar workers who could feel threatened by it? Can the later force defenders of more extended green policies to concede on points to defend certain lifestyles?

In the spectrum of possible outcomes by 2033, we first envision an extreme where these movements start to fade, and support for green policies is wavering. Given more pressing concerns, such as economic crises or geopolitical tensions, both citizens and states focus on solving those problems first, adopting mere mitigating measures against the advancement of climate change-related events, such as storm surges or floods.

Habits of consumption remain similar, and the prospects of "Green new deals" or "green jobs" either fail to accomplish their goals or are erased in favour of policies which provide short-term results.

Finally, the transition towards more usage of low-carbon energy sources is slower than expected, given that there is little policy support. And adaptation policies against the effects of climate change are adopted on an ad-hoc basis, with a reduction of climate finance.

In 2033, climate change action has become intense across all domains

On the other hand, we see a world where climate change action has become intense across all domains. On the political, not only green parties, but also other political families try to develop ambitious policies that can combine economic recovery and growth with green initiatives.

Geopolitically, there is a race to the top in climate ambition, as it is perceived to be a catalyser for technological and industrial leadership.

Social movements keep on pressing pacifically and are able to sit down with politicians of all ideologies to voice their concerns, and both SMEs and big corporations support a more sustainable economic model.

Habits of consumption change, and attitudes towards renewable and nuclear energy are positive.

To make this global win politically sustainable it will have been necessary to develop mechanisms (domestic and international) to compensate losers and pursue avenues for effectively growing, redistributing, and combatting climate action at the same time, which might have required fairly fundamental changes to the economic systems.

Note: The authors would like to thank Javier Solana for his support and guidance. We are also grateful to Joan C. Amaro, Mireia Belil, José I. Conde-Ruiz, Óscar Fernández, Xavier Ferràs, Xavier Mena, Andrés Ortega, Marc Vilanova and Marie Vandendriessche for their contributions to the individual uncertainty notes. All errors and omissions are, of course, attributable only to the authors.